The Impact of Sustainability Accounting and Reporting on Firm Value-A Case of Listed Companies on Lusaka Stock Exchange

DOI:

https://doi.org/10.5281/zenodo.10609923Keywords:

sustainability, sustainability accounting and reporting, firm value, lusaka security exchange, environmental sustainability, social sustainabilityAbstract

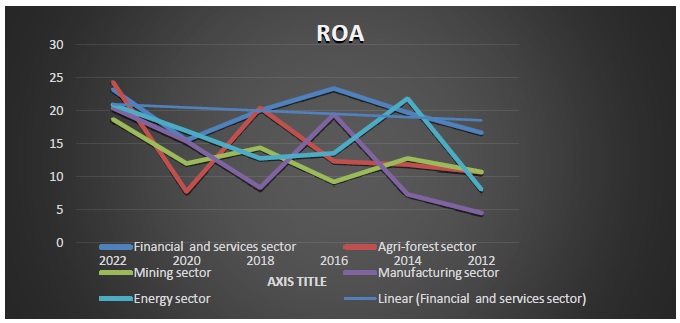

There is a growing interest among stakeholders on the subject of Sustainability Accounting and Reporting (SAR). Literature based on SAR has reviewed that there exists a relationship between SAR practices and firm value. However, this has not been confirmed on the listed companies at Lusaka Stock Exchange (LuSE). The aim of this research was to investigate the impact of SAR on firm value, focusing on companies listed on the LuSE. The Overall objective of this research was to drive positive change, improve company performance, and ensure that companies operate in a socially, environmentally and economically responsible manner. This objective was achieved by three specific objectives firstly by examining the SAR practices among LuSE listed companies in Zambia, secondly by analyzing the relationship between SAR and firm value and lastly by identification of the key drivers to implementing SAR practices among LuSE listed companies. In doing so, the study adopted a quantitative approach to collect and analyze data. The results revealed that the level of sustainability practices has been increasing over time. However there has been gaps with regards to smaller firms which are still struggling with financial stamina. It was also found that SAR has impacted firm value and overall firm performance. A weak correlation was observed which was also significantly tested at 5% confidence level. The findings indicate that a weak association between the dependent variable Return on Assets (ROA) and the independent variables that is environmental and social sustainability indicators with overall mean of 0.164 and SD= 0.169. Based on the model, it was revealed that environmental and social sustainability indicators played a pivotal role in firm value. These results show that corporate sustainability reporting index has positive and significant impact on firm performance for the listed companies on LuSE. The main drivers of SAR practices were firm size, media visibility and ownership structure and these have been important with regards to disclosure of sustainability reports, while corporate governance only seems to have an influence on the existence of audit or sustainability committees. Therefore, it was recommended that there is need to educate and improve SAR awareness among LUSE listed companies and beyond in order to achieve sustainable development for all stakeholders.

Downloads

References

Abhayawansa, S. (2022). Directions for future research to steer environment, social and governance (ESG) investing to support sustainability: A systematic literature review. Handbook of Accounting and Sustainability.

Aboud, A. (2018). The impact of social environmental and corporate governance disclosures on firm value: Evidence from Egypt. Journal of Accounting in Emerging Economies, 8(4), 442-458.

Afrooz, A. K. a. Z. (2019). The effect of the esg score on stock price jumps. Umea: Umea University-Scholl of Business Studies.

Brundtland, G. H. (1987). Report of the world commission on environment and development: Our common future. Oslo: United Nations.

Csiszko, R. S.-W. a. C. (2022). www.denxpertsolutions.com. Accessed on: 16 January 2023.

Dave, A. (2016). Global reporting initiative. Sustainability reporting Singapore, Newcastle University.

Dr. Prackasita. (2019). Firm value.

Dumitru, m. m. (2015). Marketing communications of value creation in sustainable organizations. Encostor, 17(40), 955-976.

Elkinton, J. (1999). The triple bottom line: What is it and. Indiana University Kelley School of Business, Indiana Business Research Center.

Ephraim, K. S. (2022). The value relevance of sustainability reporting: does assurance and the type of assurer matter?. Sustainability Accounting, Management and Policy Journal, 13(4), 858-877.

EY Zambia. (2022). Sustainability report. Lusaka: EY Zambia.

Frank, S. O. (2018). Disclosure of csr performance and firm value. Sustainability, 10.

Hvidkjær, S. (2017). ESG investing: A literature review.

Kam, T. (2017). A literature review on environmental, social and governance reporting and its impact on financial performance. Sustainability, 1(4), 1016.

Keddle, L. (2021). https://theconversation.com/africa. [Online]

Available at: https://theconversation.com/what-is-sustainability-accounting-what-does-esg-mean-we-have-answers-150996. Accessed on: 28 December 2022.

Khan. (2020). Sustainability accounting and reporting in the industry 4.0. Journal of Cleaner Production, 258, 120783.

Ozili, P. (2022). Sustainability accounting. SSRN Electronic Journal.

Lamberton, G. (2005). Sustainability accounting—A brief history and conceptual framework. Science Direct, 29(1), 7-26.

Lawrence., T. a. Y. W. (2017). Sustainability reporting and firm value: Evidence from Singapore listed companies. Sustainability, 9.

Lawrence, l. (2017). Sustainability reporting and firm value: Evidence from Singapore listed companies. Sustainability, 9.

LuSE. (2023). Lusaka Stock Exchange. Available at: https://luse.co.zm/listed-companies/#. Accessed on: 22 August 2023.

Marone, H. (2003). Small African stock markets-The case of the Lusaka stock exchange. International Monetary Fund.

McCartney, P. (2022). Available at: https://www.icsi.edu/media/portals/0/grapes/Sustainability%20&%20Reporting%20Series-8.pdf. Accessed on: 26 December 2022].

Muwowo. (2006). Investigation into corporate social reporting in Zambia. London: London South Bank University.

Nyeadi, J. D. (2018). Corporate social responsibility and financial performance nexus Empirical evidence from South African. Journal of Global Responsibility, 9(3), 301-328.

Ozili, P. (2022). Sustainability accounting. SSRN Electronic Journal.

Roberts, d. a. K. (2007). Sustainability reporting practices in Portugal: Greenwashing or triple bottom line?. International Business & Economics Research Journal, 6(9).

Sakuwaha, S. (2020). AGM season 2022: ESG Disclosures + Reporting. Corporate Governance Finance Services.

Sakuwaha, S. (2020). Moira mukuka legal practioners. [Online]

Available at: https://www.lexology.com/library/detail.aspx?g=6ffc619f-42d4-4317-a540-5039b7ddad9e

Accessed on: 31 December 2022.

Slaper, t. a. H. (2011). The triple bottom line: What is it and how does it work. Available at: http://www.ibrc.indiana.edu/ibr/2011/spring/article2.html. Accessed on: 09 December 2023.

Schuman, m. (1995). Managing legitimacy: Strategic and institution approaches. Academy of Management Review, 20(3), 571-610.

Swarnapali, N. (2018). Corporate sustainability reports and firm value: Evidence from a developing country. Sri Lanker: ResearchGate.

Untung, h. i. (2015). Corporate social performance and firm value. International Journal of Business and Management Invention, 4(11), 69-75.

Woo Sung Kim, K. P. I. a. S. H. L. (2018). Corporate social responsibility, ownership structure, and firm value: Evidence from Korea. Sustainability, 10.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Hilton Chinyonga, Bupe Getrude Mwanza

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'Management Journal for Advanced Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.