Effect of Whistleblowing Mechanisms on Tax Remittances Fraud Prevention of Ministries, Departments and Agencies (MDAS) in Northeast Nigeria

DOI:

https://doi.org/10.5281/zenodo.15303488Keywords:

whistleblowing, tax remittance fraud, MDAs, northeast nigeria, fraud preventionAbstract

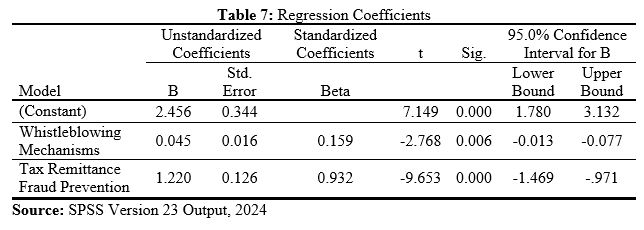

This study investigates the effect of whistleblowing mechanisms on tax remittance fraud prevention among Ministries, Departments, and Agencies (MDAs) in Northeast Nigeria. The study is grounded in the Fraud Triangle Theory, which posits that fraud is most likely when perceived pressure, opportunity, and rationalization co-exist. The research addresses a critical gap in existing literature by focusing on whistleblowing as a strategic tool to prevent tax remittance fraud in public institutions, particularly in conflict-prone and institutionally fragile regions. Utilizing a survey research design, data were collected from 290 tax personnel in 259 MDAs across six Northeastern states. The study employed regression analysis using SPSS Version 23 to determine the statistical relationship between whistleblowing mechanisms and fraud prevention. Results indicate a strong positive correlation (r = 0.667, p < 0.01) between effective whistleblowing structures and reduced tax fraud incidents. The regression analysis further revealed that whistleblowing mechanisms significantly contribute to enhancing transparency and accountability in tax remittance processes. However, multicollinearity was detected, suggesting some overlap with other anti-fraud strategies. The study concludes that institutionalized whistleblowing, supported by legal protection and cultural shifts, is essential to reducing tax fraud in Nigeria’s public sector. It recommends strengthening whistleblower protection laws, increasing public awareness and embedding whistleblowing frameworks into the financial architecture of MDAs. Future research should explore whistleblowing in other public sectors, assess long-term impact, and include comparative studies with other regions for broader insights.

Downloads

References

Adegbie, F. F., & Fakile, A. S. (2023). Whistleblowing and financial irregularities in Nigerian public institutions. Journal of Public Sector Governance, 9(2), 98–115.

Adeyemi, S. B., & Fagbemi, T. O. (2023). Anti-fraud mechanisms and financial transparency in public agencies. African Journal of Accounting and Finance, 15(1), 43–57.

Ajibola, R., & Olamide, T. (2023). Demographic dynamics and organizational performance in Nigerian public service. Nigerian Journal of Public Administration, 12(1), 77–89.

Albrecht, W. S., Albrecht, C. O., Albrecht, C. C., & Zimbelman, M. F. (2019). Fraud examination. (6th ed.). Cengage Learning.

Alleyne, P., Hudaib, M., & Pike, R. (2018). Towards a conceptual model of whistle-blowing intentions among external auditors. The British Accounting Review, 50(3), 216–231.

Alzeban, A. (2022). Internal audit and whistleblowing: A study in the public sector. International Journal of Public Sector Management, 35(4), 512–528.

Association of Certified Fraud Examiners. (2020). Report to the nations: 2020 global study on occupational fraud and abuse. ACFE.

Brennan, N. M., & Kelly, S. (2022). Enhancing corporate transparency through whistleblowing policies. Corporate Governance International Journal, 22(3), 337–355.

Chukwuma, O., Lawal, A., & Ibrahim, M. (2024). Age demographics and professional productivity in Nigeria’s MDAs. Journal of Development and Policy Studies, 19(2), 123–139.

COSO. (2013). Internal control – Integrated framework. Committee of Sponsoring Organizations of the Treadway Commission.

Creswell, J. W., & Creswell, J. D. (2018). Research design: Qualitative, quantitative, and mixed methods approaches. (5th ed.). Sage Publications.

Cressey, D. R. (1953). Other people's money: A study in the social psychology of embezzlement. Free Press.

Dyck, A., Morse, A., & Zingales, L. (2010). Who blows the whistle on corporate fraud? The Journal of Finance, 65(6), 2213–2253.

Enofe, A. O., Okpako, P. O., & Atube, E. N. (2017). The impact of forensic accounting on fraud detection. European Journal of Business and Management, 9(6), 44–52.

Gao, J., Greenberg, R. R., & Wong-On-Wing, B. (2015). Whistleblowing mechanism effectiveness: Anonymity and reporting intentions. Journal of Accounting and Public Policy, 34(4), 461–480.

Gepp, A., Linnenluecke, M. K., O’Neill, T. J., & Smith, T. (2018). Big data techniques in auditing research and practice. Journal of Accounting Literature, 40, 102–115.

Haire, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2017). Multivariate data analysis. (7th ed.). Pearson Education.

Khan, A., & Zahid, S. (2023). Fiscal reforms and fraud control in public financial management. Pakistan Journal of Finance, 14(1), 61–79.

KRA. (2021). Annual tax performance report 2021/2022. Kenya Revenue Authority.

Mesmer-Magnus, J. R., & Viswesvaran, C. (2005). Whistleblowing in organizations: An examination of correlates of whistleblowing intentions. Journal of Business Ethics, 62(3), 277–297.

Modugu, K. P., & Anyaduba, J. O. (2013). Forensic accounting and financial fraud in Nigeria. Asian Journal of Management Sciences, 1(7), 1–19.

Near, J. P., & Miceli, M. P. (1985). Organizational dissidence: The case of whistle-blowing. Journal of Business Ethics, 4(1), 1–16.

Near, J. P., & Miceli, M. P. (2016). After the wrongdoing: What managers should know about whistleblowing. Business Horizons, 59(1), 105–114.

Nwachukwu, E., & Bello, T. (2022). Talent attrition in public service: The case of aging workforce in Nigeria. Nigerian Public Administration Review, 13(2), 94–112.

O’Brien, R. M. (2007). A caution regarding rules of thumb for variance inflation factors. Quality & Quantity, 41(5), 673–690.

Ogbu, O. (2017). Whistleblowing policy implementation in Nigeria: Challenges and prospects. Nigerian Journal of Administrative Sciences, 10(1), 29–44.

Ogunyomi, P. O., & Asaolu, T. O. (2022). Tax governance and whistleblowing frameworks in Nigerian public institutions. African Journal of Taxation and Policy, 9(2), 83–99.

Okafor, A. C., Uchenna, O., & Musa, M. (2024). Institutionalizing whistleblowing practices in Nigerian public agencies. International Journal of Public Sector Management, 37(1), 49–66.

Okoye, E. I., & Gbegi, D. O. (2013). Forensic accounting: A tool for fraud detection and prevention in the public sector. International Journal of Academic Research in Business and Social Sciences, 3(3), 1–19.

Otusanya, O. J. (2011). The role of tax authorities in tackling tax evasion and avoidance. African Journal of Accounting, Auditing and Finance, 1(2), 84–107.

Oyedele, T. (2016). Strengthening Nigeria’s tax administration for economic sustainability. PwC Nigeria Policy Brief, 2(1), 3–10.

Oyedokun, G. E. (2016). Forensic accounting as a tool for fraud detection and prevention in the public sector. The Nigerian Accountant, 49(2), 18–27.

Rezaee, Z., & Wang, J. (2019). The impact of forensic accounting on fraud detection. Journal of Forensic and Investigative Accounting, 11(1), 287–306.

SARS. (2022). Annual performance plan 2021/22. South African Revenue Service.

Saha, A., Aggarwal, R., & Bansal, P. (2021). Combating corruption through whistleblowing: Evidence from developing economies. Journal of Business Ethics, 170(3), 561–576.

Yusuf, H., & Bello, K. (2024). Data integrity and fraud prevention frameworks in African tax systems. Journal of African Public Finance, 12(1), 49–67.

Zhang, Y., Nwankwo, C. O., & Umeh, E. (2023). Employee reporting behavior and anti-fraud controls in public finance. Journal of Financial Crime, 30(4), 893–910.

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Adamu Maina Sule, Sunday Mlanga, Francis Chinedu Egbunike

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'Management Journal for Advanced Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.