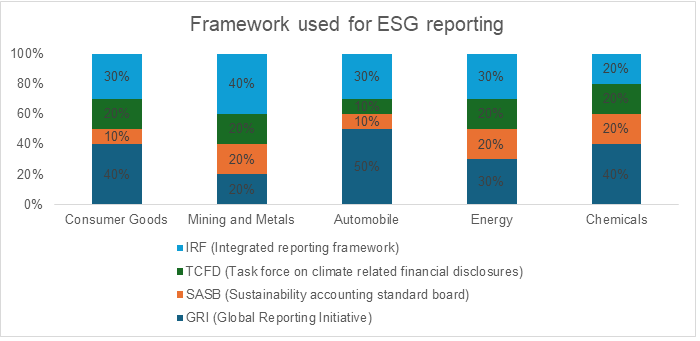

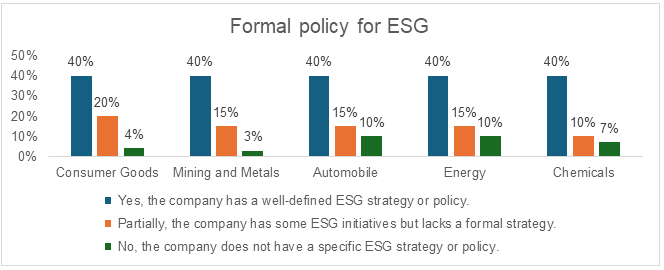

across various industries, highlighting the challenges and opportunities that companies face in this evolving landscape. Our findings underscore the importance of ESG factors in corporate decision-making and the need for robust frameworks and standards to guide ESG reporting. The Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB), and Task Force on Climate-related Financial Disclosures (TCFD) provide valuable guidelines that help ensure transparency, comparability, and accountability in ESG reporting. However, the adoption and effectiveness of these frameworks can vary significantly across industries, influenced by sector-specific challenges and regulatory environments.

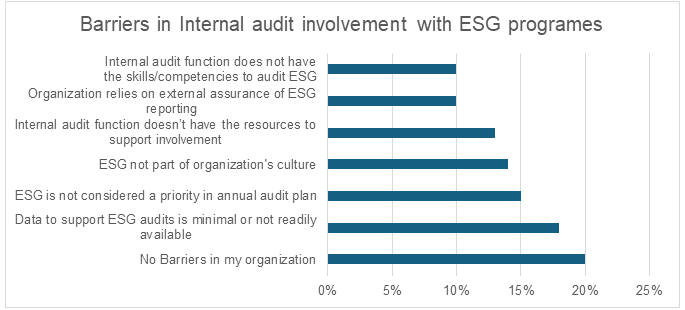

The role of internal audit is pivotal in ensuring the accuracy and reliability of ESG disclosures. Internal auditors provide independent assurance on ESG-related controls and processes, identify and mitigate ESG risks, and help organizations meet regulatory requirements and stakeholder expectations. Despite these contributions, internal auditors face barriers such as limited data availability, low prioritization of ESG in audit plans, and resource constraints.

The introduction of the Business Responsibility and Sustainability Report (BRSR) in India marks a significant step toward enhancing ESG reporting and fostering sustainable business practices. The mandatory adoption of BRSR for the top 1000 listed entities by market capitalization from FY 2022-23 is expected to improve the quality and consistency of ESG disclosures in India.

To further promote ESG adoption in India, there is a need for increased awareness among companies, investors, and regulators about the importance of ESG factors for sustainable and responsible investing. Companies should strive for more comprehensive and standardized disclosures, while the regulatory environment should be strengthened to promote greater ESG compliance.

In conclusion, effective ESG integration can lead to better financial performance, improved risk management, and enhanced stakeholder relations. By addressing the challenges and leveraging the opportunities identified in this study, organizations can enhance their ESG practices and reporting, ultimately contributing to a more sustainable and responsible corporate sector.

Way Forward:

1. To promote ESG adoption in India, there needs to be increased awareness among companies, investors, and regulators about the importance of ESG factors for sustainable and responsible investing.

2. Companies in India should providemore comprehensive and standardized disclosures on ESG factorsto enable investors to evaluate their ESG performance more effectively.

3. The regulatory environment in India should bestrengthened to promote greater ESG compliance by companies.This could involve introducing more robust reporting requirements, establishing clearer ESG standards, and enforcing regulations more rigorously.

References

1. Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835-2857.

2. Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance & Investment, 5(4), 210-233.

3. Institute of Internal Auditors (IIA). (n.d.). The IIA’s three lines model: An update of the three lines of defense.

4. KPMG. (2021). ESG reporting in India: Building trust and credibility.

5. PwC. (2020). ESG reporting: Getting started with reporting ESG information.

6. Sustainability Accounting Standards Board (SASB). (n.d.). Standards overview.

7. Task Force on Climate-related Financial Disclosures (TCFD). (2017). Recommendations of the task force on climate-related financial disclosures.

8. Clark, G. L., Feiner, A., & Viehs, M. (2015). From the stockholder to the stakeholder: How sustainability can drive financial outperformance. University of Oxford and Arabesque Partners.

9. Global Reporting Initiative (GRI). (2016). GRI standards. Retrieved from: https://www.globalreporting.org/

©

©