Comparative Study of Financial Planning Habits among Students and Salaried-Employed Individuals in Kolkata

Ghanti N1*, Saha A2

DOI:10.5281/zenodo.17010747

1* Nirjhar Ghanti, Under Graduate Student, Department of Management, Institute of Leadership, Entrepreneurship and Development (iLEAD), Kolkata, West Bengal, India.

2 Arijit Saha, Assistant Professor, Department of Management, Institute of Leadership, Entrepreneurship and Development (iLEAD), Kolkata, West Bengal, India.

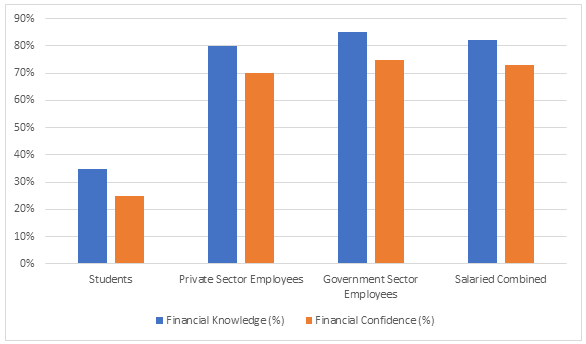

Despite the increasing significance of financial literacy, there is a deficiency of thorough research that juxtapose the financial behaviors of students and salaried professionals in an urban setting such as Kolkata.This study seeks to address this deficiency by offering a comprehensive comparison of the financial planning practices and investment behaviors of these two cohorts. It aims to comprehend the obstacles they have regarding financial literacy, decision-making, and their overall financial health.This study employs a descriptive, quantitative, cross-sectional research approach. The findings of this study provide valuable insights into the financial behaviors, challenges, and financial literacy levels of students and salaried employees in Kolkata.

Keywords: financial planning, personal finance, financial behavior

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Under Graduate Student, Department of Management, Institute of Leadership, Entrepreneurship and Development (iLEAD), Kolkata, West Bengal, India. Email:  |

Ghanti N, Saha A, Comparative Study of Financial Planning Habits among Students and Salaried-Employed Individuals in Kolkata. Manag J Adv Res. 2025;5(4):10-16. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/229 |

|

©

©