Forensic Accounting - A Game Changing Approach for Holistic Corporate Sector Development in India

Gupta PK1

DOI:10.54741/mjar.2.6.7

1 Pawan Kumar Gupta, Assistant Professor, Department of Commerce, Mggac, Mahe, India.

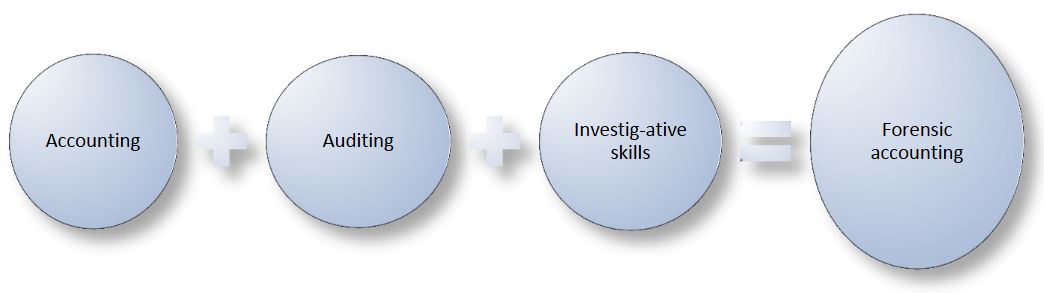

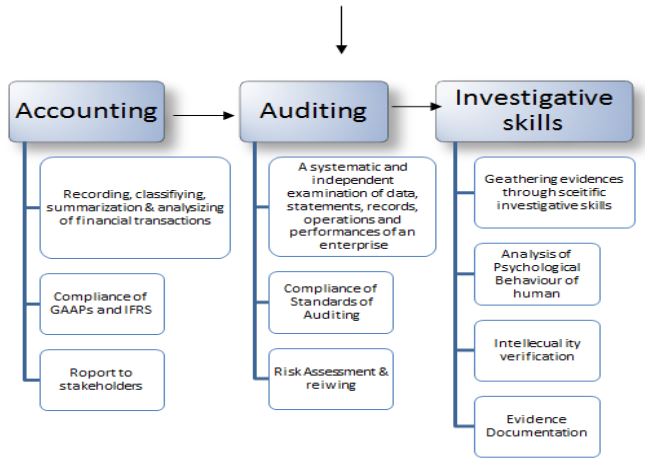

Forensic accounting is the prominent instrument in the field of accounting area to tackle the rampant situation of financial fraud. Forensic accounting is a specific branch of accounting. It involves the application of special skills such as accounting, auditing procedures, finance, quantitative methods, research, and investigations in accounting activities. With the rapid growth of technology in India after globalization, the trend of accounting is also changing as per the demand of stakeholders due to facing these complex natures of fraud. Forensic accounting is one of the transcendent examples in the area of accounting. It is capable to find out all kinds of fraud; if we use it attentively. The techniques of forensic accounting are also developing with the need of time. Modern technologies are more powerful in comparison to conventional technologies. In the dynamic cyber world, the complex natures of frauds are creating a need for research in the forensic accounting area. Since independence, the Incremental growth of voluminous financial scams is a black spot in the Indian economy. Moreover, the list of challenges to better practices of forensic accounting in India is too extensive. There are few agencies in India, which are dedicated to the mission of combating fraud for example- SFIO, FEMA, RBI, CBI (Economic Office Wing) deals with big financial scams, Central Vigilance Commission deals with corruption. In view of India, the better practices of forensic accounting should be observed by stakeholders carefully to boost economic growth.

The present study discusses the conceptual framework of forensic accounting, the implementation & progress of forensic accounting, the authorities involved, and suggestions for better implementation of forensic accounting from the Indian perspective.

Keywords: forensic accounting, dynamic cyber world, financial fraud, indian economy

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Assistant Professor, Department of Commerce, MGGAC, MAHE, , India. Email:  |

Gupta PK, Forensic Accounting - A Game Changing Approach for Holistic Corporate Sector Development in India. Manag. J. Adv. Res.. 2022;2(6):39-45. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/43 |

|

©

©