A Study on Financial Performance of Motilal Oswal Ltd.

Manjunath1, Sathvik S2*

DOI:10.5281/zenodo.17097646

1 Manjunath, MBA Student, Department of Management Studies, Ballari Institute of Technology and Management (Autonomous Institute under VTU-Belagavi), Jnana Gangothri Campus, Allipur, Hospet Road, Ballari, Karnataka, India.

2* Sathvik S, Associate Professor, Department of Management Studies, Ballari Institute of Technology and Management (Autonomous Institute under VTU-Belagavi), Jnana Gangothri Campus, Allipur, Hospet Road, Ballari, Karnataka, India.

Financial performance is a critical aspect of any organization, reflecting its ability to generate earnings and sustain itself over time. At its core, financial performance is a measure of how well an organization utilizes its resources to generate revenue, manage costs, and create value for its stakeholders. The theoretical background of financial performance is rooted in various financial theories and concepts, including the Efficient Market Hypothesis (EMH), Agency Theory, and Signaling Theory. These theories provide insights into how financial performance is influenced by factors such as market efficiency, agency costs, and information asymmetry. Financial performance refers to how well a company manages its assets, liabilities, and overall financial health to generate revenue and achieve profitability. It's a comprehensive evaluation of a company's financial standing, encompassing its ability to utilize resources, manage debts, and generate profits.

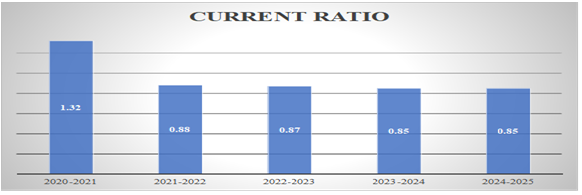

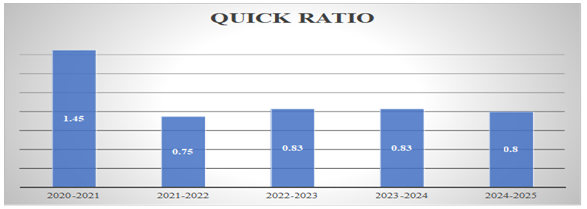

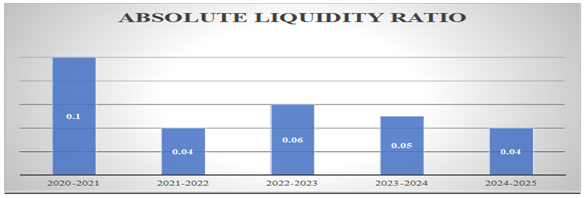

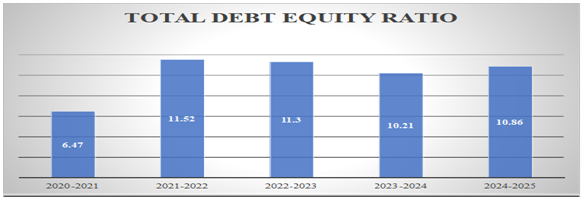

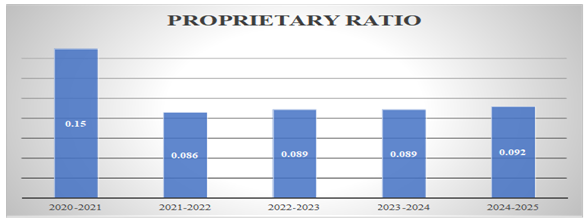

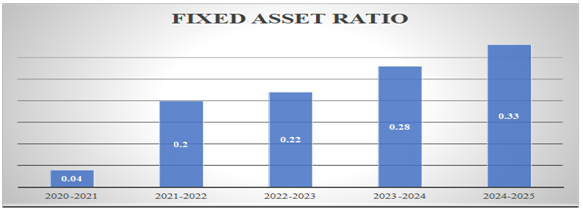

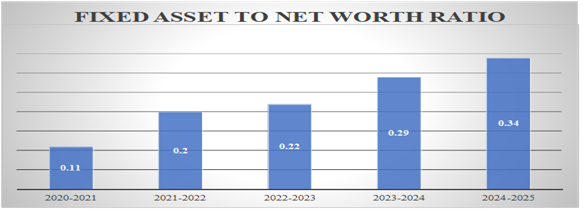

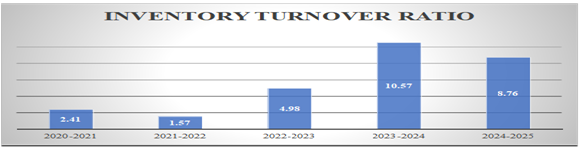

Objectives of the Study: The objectives of the present research is to analyze the financial performance of Motilal Oswal limited using key financial ratio, Examine the liquidity and solvency position of Motilal Oswal limited, To examine the impact of debt implications on shareholders networth and also to evaluate overall financial performance using dupont analysis.

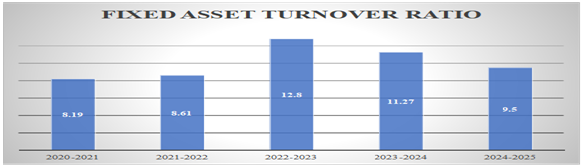

Research Methodology: The Present study is based on secondary data.. To gather the relevant information, such as the net profit, total revenue, and working capital, the financial data from the companies five-year financial statements has been utilised. From the year 2020 to 2024 data and secondary data has been collected from research articles published in journals of repute, besides this authors have collected data from capital line database and authentic e-sources such as money control.com, ticker finology sources are utilised. Ratio analysis is the financial tool used to determine the key financial performance of Motilal Oswal Ltd.

Principal Findings of the study: Effective and efficient financial performance is critical to the survival and increased profitability of any firm. Analyzing financial performance is crucial for determining the company's profitability and potential risks. Company's long-term debt to shareholders' net worth ratio has increased significantly over the years. In 2020-2021, the ratio was 0.27, indicating that long term debt was approximately 27% of shareholders' net worth.

Keywords: financial performance, ratio analysis, financial statements, profitability, shareholders networth, debt-equity ratio

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Associate Professor, Department of Management Studies, Ballari Institute of Technology and Management (Autonomous Institute under VTU-Belagavi), Jnana Gangothri Campus, Allipur, Hospet Road, Ballari, Karnataka, India. Email:  |

Manjunath, Sathvik S, A Study on Financial Performance of Motilal Oswal Ltd.. Manag J Adv Res. 2025;5(4):71-80. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/245 |

|

©

©