Financial Capability (FC): A Systematic Review of Literature and Prospects for Future Research

Mallick M1*, Das S2

DOI:10.5281/zenodo.17068018

1* Moupiya Mallick, Research Scholar, Faculty of Management, JIS University, Kolkata, West Bengal, India.

2 Sulagna Das, Associate Professor, Faculty of Management, JIS University, Kolkata, West Bengal, India.

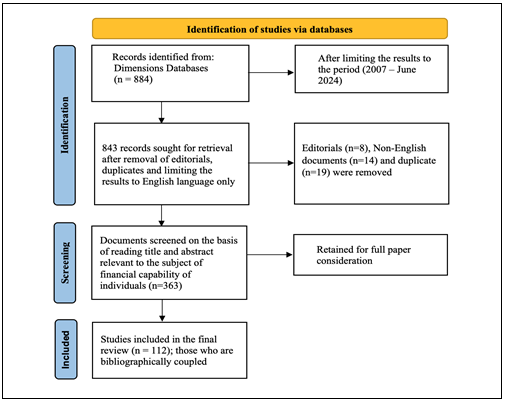

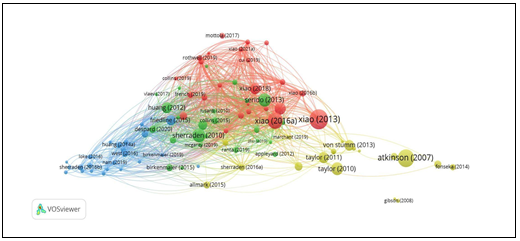

The available research literatures concerning the emerging area of financial capability demonstrates a broad range of perspectives on both the definition and assessment of this concept. Although there is an ample amount of research literature available for reviewing measurement domains and indicators, there is a lack of extensive bibliographic analysis in this area. The primary objective of this study is to pinpoint major contributors, focal areas, existing dynamics, and propose potential avenues for future research within this specific domain. The systematic literature review (SLR) adheres to the protocol outlined in the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA). This study employs a methodological approach involving systematic literature review, alongside bibliometric, network, and content analysis. This scoping review conducted an analysis of scholarly literature on financial capability from the years 2007 to 2023. In total, 363 studies satisfied all the inclusion criteria for the present study. Utilizing bibliometric techniques, four distinct research clusters have been discerned, and an in-depth content analysis has been conducted on the papers associated with these clusters. The predominant research emphasis in this field revolves around impact of financial capability on financial satisfaction and financial well-being followed by it’s impact on financial behaviour. Subsequently, the focus extends to influence of financial education on financial capability and the measurement of its level. Later part of this study includes recommendations regarding the standardization of measurement for the components within financial capability and the assessment of financial capability itself.

Keywords: financial capability, financial knowledge, financial behaviour, financial opportunity, systematic literature review, bibliometric analysis, network analysis, content analysis

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Research Scholar, Faculty of Management, JIS University, Kolkata, West Bengal, India. Email:  |

Mallick M, Das S, Financial Capability (FC): A Systematic Review of Literature and Prospects for Future Research. Manag J Adv Res. 2025;5(4):55-70. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/241 |

|

©

©