Determinants of Financial Well Being: A Study of Urban Working Women in West Bengal

Bhattacharjya P1*, Chatterjee S2, Jha NK3

DOI:10.5281/zenodo.17060279

1* Patralika Bhattacharjya, Research Scholar (Ph.D), Department of Economics, Sister Nivedita University, Kolkata, West Bengal, India.

2 Susmita Chatterjee, Assistant Professor, Department of Economics, Maharaja Manindra Chandra College, Kolkata, West Bengal, India.

3 Navin Kumar Jha, Professor and HOD, Department of Economics, Sister Nivedita University, Kolkata, West Bengal, India.

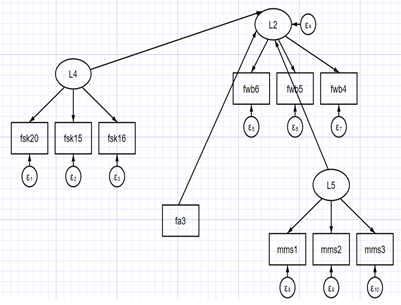

This study investigates the facilitating role of Financial Skills and Financial Autonomy on Financial Well Being of Urban Working Women in West Bengal. In the methodology of the research study, a primary survey was carried out in a cross-sectional manner and 332 participants were studied. It investigates the structural covariance among latent factors like Financial Autonomy, Financial Skill (FSK), Financial Well-being (FWB), and Money Management Stress (MMS) through Structural Equation Modelling (SEM). The questionnaire comprised of validated questions that evaluated the constructs of interest, and it was developed through a literature review of financial behaviour and psychological well-being found in Behavioural Economics Literature. The final SEM model consisted of three latent variables as per a well-established theoretical framework. The findings indicate that Financial Skills in combination with Financial Autonomy or the ability of an individual to independently manage their finances, make informed financial decisions, and take effort towards their own financial goals emphatically increases Financial Well Being and reduces Money Management Stress in Urban Working Women.

Keywords: financial autonomy, financial skills, financial well being, money management stress, urban working women

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Research Scholar (Ph.D), Department of Economics, Sister Nivedita University, Kolkata, West Bengal, India. Email:  |

Bhattacharjya P, Chatterjee S, Jha NK, Determinants of Financial Well Being: A Study of Urban Working Women in West Bengal. Manag J Adv Res. 2025;5(4):48-54. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/240 |

|

©

©