Digital Financial Inclusion and Self-Help Groups in India: A Theoretical Review into Empowerment, Credit Linkage, and Sustainable Development

Rao AN1, Ramishah2, Sarkar B3, Basu U4*

DOI:10.5281/zenodo.16447073

1 Ayushee N Rao, Student of Bachelor of Commerce (3rd year), Department of Commerce, Adamas University, Kolkata, West Bengal, India.

2 Ramishah, Student of Bachelor of Commerce (3rd year), Department of Commerce, Adamas University, Kolkata, West Bengal, India.

3 Bharat Sarkar, Student of Bachelor of Commerce (3rd year), Department of Commerce, Adamas University, Kolkata, West Bengal, India.

4* Uttiya Basu, Assistant Professor, Department of Commerce, Adamas University, Kolkata, West Bengal, India.

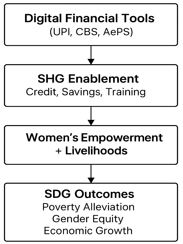

Introduction: Over the past few years, self-help organizations have advanced in the Indian economy thanks in large part to digital financial inclusion. Through the many facets of the digital financial inclusion process, the Joint Liability Groups (JLG) and Farmer Interest Groups (FIG) are also making progress in their social inclusion and economic growth. Point of Sale (POS) counters, Adhar-enabled payment methods, Core Banking System (CBS), and various Unified Payment Interfaces (UPI) are all playing a significant role in creating the nation's digital ecosystem and fostering a close relationship with the country's semi-urban and rural areas through digital financial inclusion.

Objective of the Study: The study's goals are to determine if the process of digital financial inclusion has any bearing on the financial advancements of Self-Help Groups (SHGs) in India and to evaluate the effects of various government initiatives implemented thus far to enhance the same. Another aspect of this study is how DFI creativity and SHGs may work together to help India achieve the SDGs.

Methodology: Information gathered from various government websites, journals, magazines, newspapers, and e-books forms the basis of the theoretical research with the case study. Additionally, this study uses quarterly NABARD reports as an additional quantitative data source.

Results: Enterprises for Digital Financial Inclusion (DFI), which have a massive potential to advance sustainable development improvements in the Indian economy, have a substantial influence on self-help groups (SHGs). The actual empowerment of Self-Help Groups (SHGs) has been transmuted by the incorporation of digital technology and financial services, which has subsequently assisted in the socioeconomic progression of communities around the world. Subsequently, this empowerment has elevated household incomes, assisted fight against poverty, and boosted living circumstances for semi-urban and rural residents.

Keywords: digital financial inclusion, economic growth, government policies, living standards, self-help groups

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Assistant Professor, Department of Commerce, Adamas University, Kolkata, West Bengal, India. Email:  |

Rao AN, Ramishah, Sarkar B, Basu U, Digital Financial Inclusion and Self-Help Groups in India: A Theoretical Review into Empowerment, Credit Linkage, and Sustainable Development. Manag J Adv Res. 2025;5(3):79-84. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/227 |

|

©

©