Perceived Effect of Tax Provisions on Nigerian Tax Administration

Gubio BM1, Hussaini I2*, Maidarasu AU3, Jajere UU4

DOI:10.5281/zenodo.16017994

1 Babagana Mali Gubio, Department of Accounting, Yobe State University, Damaturu, Nigeria.

2* Ibrahim Hussaini, Department of Accounting, Yobe State University, Damaturu, Nigeria.

3 Abubakar Umar Maidarasu, Department of Auditing and Forensic Accounting, College of Private Sector Accounting, ANAN University, Kwall, Plateau State, Nigeria.

4 Usman Umaru Jajere, Department of Auditing and Forensic Accounting, College of Private Sector Accounting, ANAN University, Kwall, Plateau State, Nigeria.

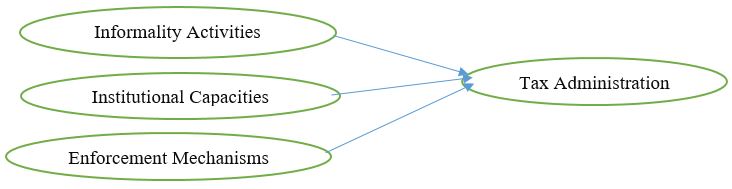

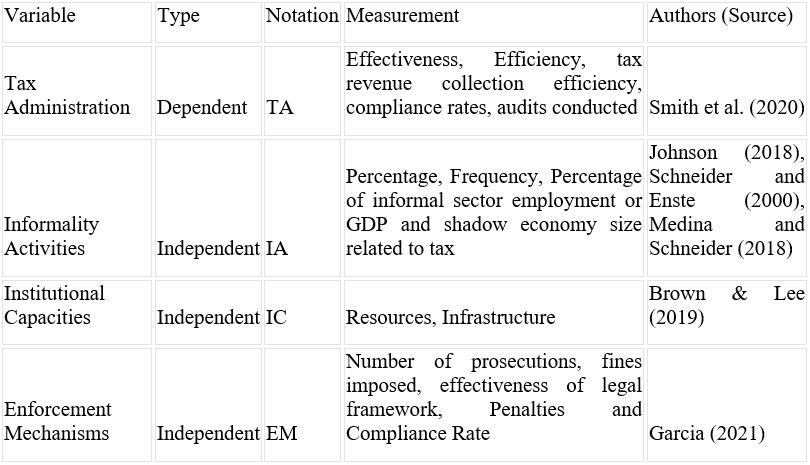

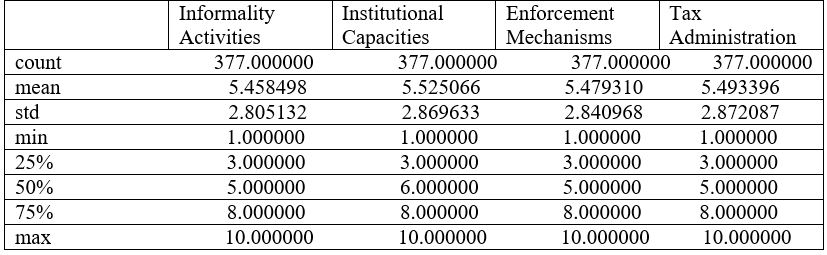

Tax provisions is an instrument which in shaping tax administration, particularly in developing countries like Nigeria. This study explores the perceived effects of tax provisions on Nigerian tax administration, considering challenges such as informality, weak institutional capacities, and enforcement mechanisms. The research employs a quantitative approach, collecting data through online surveys from a diverse sample across Nigeria's six geo-political zones. Descriptive and inferential statistical methods are used for data analysis. Findings indicate moderate levels of informality activities, institutional capacities, enforcement mechanisms, and tax administration effectiveness. However, weak correlations suggest that the relationships between these variables may not be significant, highlighting the need for further research. The study underscores the importance of understanding the nuanced dynamics between tax provisions and tax administration to address challenges and improve revenue collection in Nigeria.

Keywords: administration, effect, provisions, tax, informality

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Department of Accounting, Yobe State University, Damaturu, Nigeria. Email:  |

Gubio BM, Hussaini I, Maidarasu AU, Jajere UU, Perceived Effect of Tax Provisions on Nigerian Tax Administration. Manag J Adv Res. 2025;5(3):69-78. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/226 |

|

©

©