Enhancing Financial Literacy for Sustainable Future: A study among Kerala’s Rural Cashew Workers

Benny. C1*, S.Umaprabha2

DOI:10.5281/zenodo.15543198

1* Benny. C, Research Scholar, Department of Commerce, Thanthai Periyar Govt. Arts and Science College (Autonomous), Affiliated to Bharathidasan University, Trichy, India.

2 S.Umaprabha, Assistant Professor and Research Supervisor, Department of Commerce, Department of Commerce, Thanthai Periyar Govt. Arts and Science College (Autonomous), Affiliated to Bharathidasan University, Trichy, India.

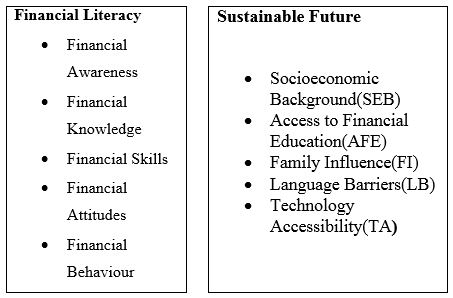

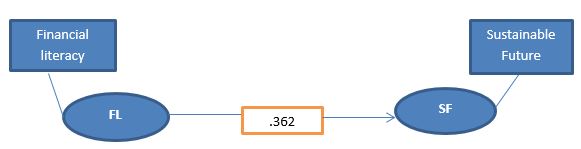

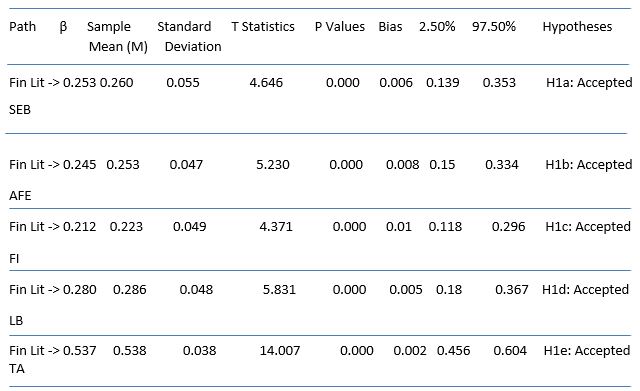

The impact of financial literacy on rural cashew workers's long-term economic security and growth is explored in this research from Kerala, India. It stresses the need of financial education in raising financial literacy, a prerequisite for economic agency. The study looks at the effects of financial literacy on leadership, time management, financial wellness, decision-making, income management, and other aspects of economic growth. This study uses Structural Equation Modelling (SEM) as part of its deductive quantitative technique to examine data collected from 426 rural cashew workers who are economically disadvantaged. The results show that there are strong links between knowing how to handle money and being financially independent in the long run. The study highlights how financial education and literacy may help rural cashew workers become more financially independent and secure, which in turn helps achieve sustainable development goals and more financial inclusion.

Keywords: financial literacy, sustainable development, economic empowerment, financial behaviour, rural cashew workers

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Research Scholar, Department of Commerce, Thanthai Periyar Govt. Arts and Science College (Autonomous), Affiliated to Bharathidasan University, Trichy, India. Email:  |

Benny. C, S.Umaprabha, Enhancing Financial Literacy for Sustainable Future: A study among Kerala’s Rural Cashew Workers. Manag J Adv Res. 2025;5(2):83-92. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/211 |

|

©

©