A Comparative Study on the Digital Services Offered by Commercial Banks and Mobile Network Operators (MNOs): A Survey of Standard Chartered Bank Lusaka Customers

Temba SM1*, Mwanza BM2

DOI:10.5281/zenodo.14942545

1* Sophia M Temba, Graduate School of Business, University of Zambia, Zambia.

2 Bupe M Mwanza, Graduate School of Business, University of Zambia, Zambia.

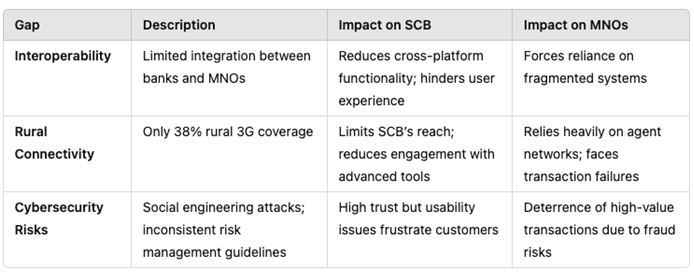

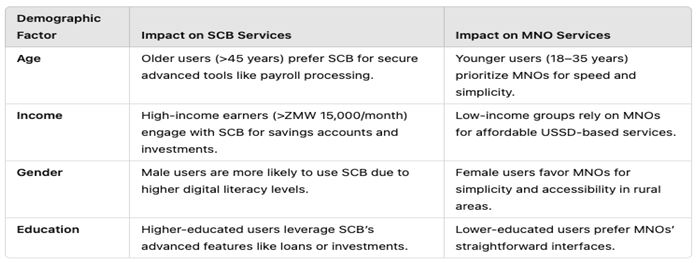

This study aimed to compare the utilization of digital financial services provided by Standard Chartered Bank (SCB) and mobile network operators (MNOs) among customers in Lusaka, Zambia, with the ultimate goal of enhancing financial inclusion. The specific objectives included analyzing usage trends, examining determinants affecting customer choices, and identifying potential improvements based on customer experiences and expectations. A mixed-methods approach was employed, combining quantitative survey data with qualitative insights. The findings revealed that MNOs were the most frequently used digital financial service providers, with 39.7% of respondents indicating a preference for services like MTN Mobile Money and Airtel Money. SCB also had a significant user base, with 36.2% of respondents utilizing its digital financial services. Convenience emerged as the most influential factor in determining customer choices, followed by security and ease of use. However, several challenges were identified, including the complexity of services, poor customer service, and lack of awareness. The study also highlighted significant differences in satisfaction levels across different income groups, suggesting that income influences perceptions of service quality. Based on the findings, the study recommends simplifying user interfaces, enhancing security measures, increasing awareness and education, improving customer support, and expanding service features to address the identified challenges and promote greater financial inclusion. These recommendations aim to guide policymakers, financial institutions, and service providers in developing more user-centric and effective digital financial solutions. The study concludes that addressing these areas can significantly improve the user experience and increase the adoption of digital financial services, thereby advancing financial inclusion in Zambia.

Keywords: digital financial services, financial inclusion, mobile network operators (mnos), standard chartered bank (scb), customer experience

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , Graduate School of Business, University of Zambia, Zambia. Email:  |

Temba SM, Mwanza BM, A Comparative Study on the Digital Services Offered by Commercial Banks and Mobile Network Operators (MNOs): A Survey of Standard Chartered Bank Lusaka Customers. Manag. J. Adv. Res.. 2025;5(1):7-24. Available From https://mjar.singhpublication.com/index.php/ojs/article/view/185 |

|

©

©

.JPG)